The Middle East and Africa external storage market declined 8.8% year-on-year during the third quarter of 2013, according to the latest figures from IDC.

The Middle East and Africa external storage market declined 8.8% year-on-year during the third quarter of 2013, according to the latest figures from IDC.

The study ‘EMEA Quarterly Disk Storage Systems Tracker’ found that external storage revenue in the region fell to $241.4 million in Q3 2013, with terabyte capacity rising some 16.6% over the same period.

”The decline can be attributed to slowdown and delay in storage investments in some of the largest markets within the region,” said Adriana Rangel, Research Director, Systems and Infrastructure Solutions, IDC Middle East, Africa, and Turkey. “However, the decline does not indicate the start of a long-term downward trend but a mere delay in impending storage market investments and upgrades.”

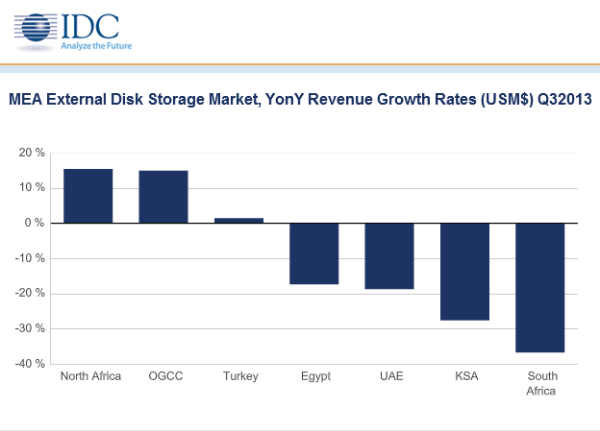

In the Middle East, the ‘other Gulf Cooperation Council’ (OGCC) group of countries, comprising Bahrain, Kuwait, Oman, and Qatar, posted healthy year-on-year growth of 15.1%, with Kuwait and Oman registering strong double-digit increases on the back of multiple public sector projects and tenders.

The UAE and Saudi Arabia, both big storage markets, witnessed year-on-year declines of 27.0% and 19.8%, respectively, in Q3 2013. “The summer months, which coincided with the holy month of Ramadan, resulted in the postponement of several projects in the Saudi oil & gas and government sectors,” Swapna Subramani, Senior Research Analyst, IDC Middle East, Africa, and Turkey said. “The UAE also saw a number of planned projects remain uninitiated during the third quarter of the year.”

The North Africa region (comprising Morocco, Algeria, and Tunisia) recorded healthy year-on-year growth of 17.6% in Q3 2013, following stability in the political and economic situation of the region and corresponding resumption in investments by the government, financial and telecommunication sectors.

South Africa suffered a major decline of 36.7% over the same period as the majority of investments that took place were typical run-rate business, in contrast to the third quarter of 2012, which was driven by numerous large projects. Predictably, Egypt’s external storage market slumped 17.3% as a result of continued political instability and uncertainty in the country.

From a protocol perspective, iSCSI experienced a healthy year-on-year surge of 12.3% in Q3 2012, driven by investments in the finance and telecommunications sectors. However, Fibre Channel retained the maximum share in terms of protocol, despite suffering a year-on-year decline in value.

From a vendor perspective, EMC continued to dominate the market with 46.1% share, which it secured by winning sizeable projects across the region. The market leader’s revenue growth, however, remained flat year-on-year. IBM posted healthy year-on-year growth, gaining share in the process to take second place with 12.8% of the market. HP and NetApp followed closely with 11.9% and 10.2% shares, respectively. Dell and Hitachi tied in fifth place in the region’s external storage market, each securing 5.9% share.